Table of Contents

Executive Summary

Kentucky has established itself as a national leader in pro-growth tax reform after landmark legislation in 2018 replaced a complex graduated income tax with a flat rate and broadened the sales tax base. These structural improvements have propelled the Commonwealth’s business tax climate ranking from 37th to 18th and built a historic Budget Reserve Trust Fund. To sustain this competitive momentum and address unprecedented workforce mobility, The Buckeye Institute used its dynamic scoring model—STELA—to model the economic effects of the next two phases of tax reform: a scheduled reduction to a 3.5 percent individual income tax rate in 2026, and a hypothetical reduction to three percent in 2027.

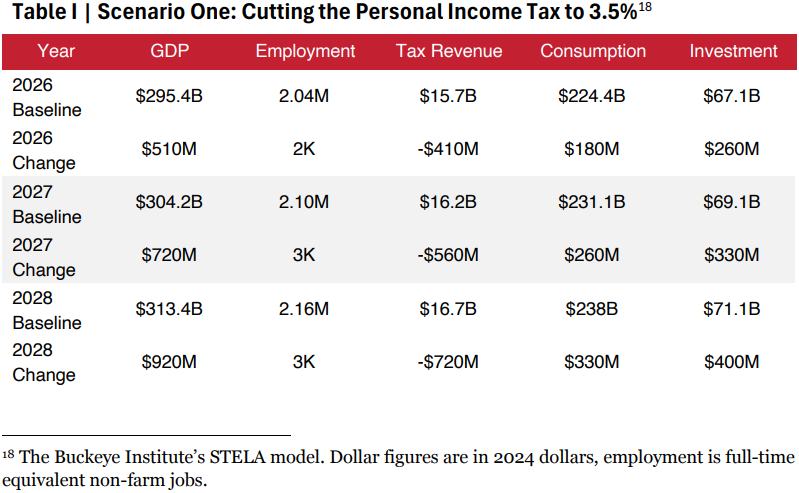

The dynamic analysis confirms that reducing taxes on labor triggers immediate economic growth. As the tax burden falls, the economy experiences a sharp acceleration in capital mobilization and labor supply. This activity generates a powerful feedback loop in which new economic growth creates new state revenue, significantly offsetting the static costs of the rate cuts. STELA forecasts that Kentucky’s growth domestic product (GDP) will grow by $510 million and private investment will surge by $260 million as capital is deployed early, reducing the static revenue loss of $718 million to a dynamic loss of just $410 million.

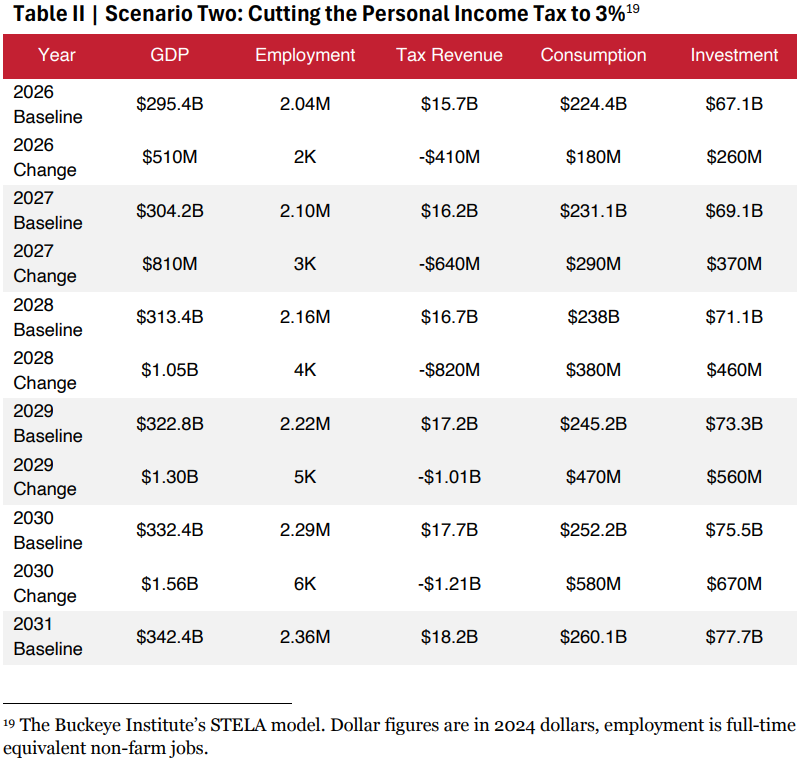

A subsequent reduction to three percent in 2027 amplifies these gains with increased business investment. Once fully implemented, the deeper tax cut raises GDP by $810 million and private investment by $370 million, containing the dynamic revenue loss to $640 million.

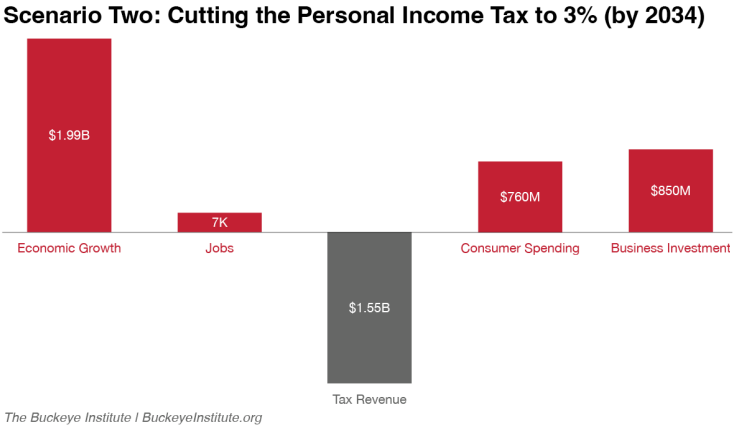

By 2034, fully phasing in the three percent flat tax will permanently elevate Kentucky’s economic baseline. STELA forecasts that annual GDP will rise by $1.99 billion, supported by $850 million in new annual investment and 7,000 new jobs. This analysis confirms that eliminating Kentucky’s personal income tax remains a fiscally responsible path to sustained growth, allowing the commonwealth to compete effectively for talent and investment in an increasingly mobile economy.

Educate your inbox. Get the Bluegrass Institute's once-weekly policy update.

Introduction

States across the country have recently pursued pro-growth tax reforms designed to flatten or eliminate their income taxes—and for good reason. Income taxes discourage work and investment and hinder productivity. Economic research routinely confirms that only corporate taxes are more damaging to growth and prosperity than personal income taxes. By taxing personal income, states inevitably influence incentives for earning that income: the less income that earners may keep, the less incentive they have to earn it. Internationally, a 10 percent reduction in the marginal income tax rate increased the employment rate in the average Organisation for Economic Co-operation and Development (OECD) country by 3.7 percentage points, while domestically, state taxes here reduce personal income over the long-term as negative economic incentives accumulate.

Acknowledging that economic reality, Kentucky made a bold, necessary policy move with landmark legislation in 2018 that converted its complex graduated income tax into a single, flat-rate tax of five percent and strategically broadened the sales tax base to fund the initial rate reduction responsibly. Subsequently, House Bill 8 in 2022 began continuous rate reductions designed to phase out the individual income tax entirely. These structural changes have proven dramatically successful, fueling consecutive record-breaking budget surpluses and propelling Kentucky’s national tax ranking from 37th in 2018 to a more competitive 18th by 2024.

A measure of this success, Kentucky’s General Fund revenue rose 2.8 percent to $15.57 billion in fiscal year 2024, as the state’s personal income tax, sales tax, and use tax each contributed approximately 37.3 percent to the total fund. Individual income tax collections settled at $5.81 billion, a slight 0.6 percent decline driven by the reduction in the statutory tax rate, while sales and use tax receipts rose to $5.80 billion on the strength of 4.1 percent growth in consumer spending. Business taxes also performed well, with corporate income and limited liability entity tax revenue climbing 2.3 percent to $1.25 billion (eight percent of the total). These totals, along with other smaller tax receipts, have raised Kentucky’s Budget Reserve Trust Fund to $3.76 billion, and reached the revenue triggers needed for the next phase of reform. Accordingly, the Kentucky legislature passed House Bill 1 (2025), which will reduce the income tax rate from four to 3.5 percent in 2026 as a pure tax cut paid for by the commonwealth’s own economic success.

And Kentucky’s success looks poised to continue. Using its dynamic analytical tool, The Buckeye Institute has modeled the economic impact of two pro-growth tax reform scenarios: (1) Kentucky’s scheduled personal income tax rate reduction from four to 3.5 percent in 2026, and (2) an additional hypothetical, trigger-based reduction from 3.5 to three percent in 2027. Both scenarios will unleash significant economic growth, boost private-sector investment, increase personal consumption, and create new jobs across the commonwealth.

Competitive Tax Policy Matters

Having a competitive state tax code matters when trying to retain residents and attract new businesses and workers. States with above-average income tax rates tend to lose population to other states compared to those with lower tax rates, and high progressive income taxes are more likely to drive investment and relocation decisions of successful businesses and workers. Higher taxes on high incomes raise less revenue than anticipated, as more affected taxpayers leave the state and reduce the overall tax base. Such emigration shrinks present and future tax revenues and economic growth, compounding the harm. With high-skilled workers and businesses more mobile now than ever, Internal Revenue Service data confirms significant transfers of taxpayers and income from high-tax to low-tax states. 14 Fortunately, Kentucky’s flat-tax move has already proven advantageous, yielding net population gains in the fight for new residents.

But that fight is far from over. The Tax Foundation’s 2026 State Tax Competitiveness Index shows that as other states accelerate their own reforms, Kentucky’s now ranks 25th overall. The commonwealth faces critical economic competition from its neighbors, most notably zero-tax Tennessee (ranked 8th) and low-tax Indiana (ranked 10th). And earlier in 2025, Ohio adopted a flat tax with a top tax rate of 2.75 percent, one of the lowest in the country. To meet the competitive challenge, Kentucky will need further responsible tax reform and prudent fiscal management. The commonwealth’s historic surpluses are not merely a defense against economic downturns but offer strategic assets that provide the state with the economic flexibility to invest in pro-growth reforms that will keep more money in the private sector and make Kentucky’s economy more dynamic and competitive.

As Kentucky policymakers consider and pursue viable reforms, they should remember that tax codes should be simple, transparent, neutral, and stable. A simple tax code means that businesses and individuals can spend less time and money on compliance costs, and taxpayers make fewer honest mistakes in their tax filings. A transparent tax code means fewer tax gimmicks, credits, and deductions that reward crony capitalism and special-interest lobbying. A neutral tax code means taxpayers pay the same rate for the same economic activity and their savings are not penalized with multiple investment taxes. And a stable tax code reduces uncertainty, allowing businesses and workers to plan effectively. Kentucky’s plan to continue reducing its flat tax rate to zero aligns with these goals and maintains a low rate across a broad base.

Modeling the Economic Impact of Tax Cuts

Scenario 1: Cutting the Personal Income Tax to 3.5%

Scenario 1 models the personal income tax cut from four to 3.5 percent, which took effect on January 1, 2026. The results demonstrate a distinct unlocking effect immediately upon implementation. As the tax burden is reduced, the economy experiences a sharp initial surge in capital mobilization, with investment jumping by $260 million and GDP rising by $510 million in 2026 alone (See Table I). This immediate release of economic activity generates significant dynamic feedback.

Following this initial acceleration, the economy grows at a permanently higher level due to the structural improvement in the tax code. By 2034, the sustained incentives are expected to lift annual GDP by $1.76 billion, boost investment by $750 million, and increase consumer spending by $670 million. While the static revenue cost grows over time, this long-term expansion provides a durable offset, supporting the creation of 6,000 new jobs by 2034.

Scenario 2: Cutting the Personal Income Tax to 3.0%

Scenario 2 models the next potential step in Kentucky’s pro-growth reform: a hypothetical reduction of the personal income tax rate from 3.5 percent to three percent. This scenario assumes the state meets its fiscal triggers again, immediately following the 2026 implementation, which would authorize the rate to fall to three percent in 2027. Upon implementation in 2027, the economy responds immediately, with GDP rising by $810 million and private investment increasing by $370 million in the first year alone (See Table II).

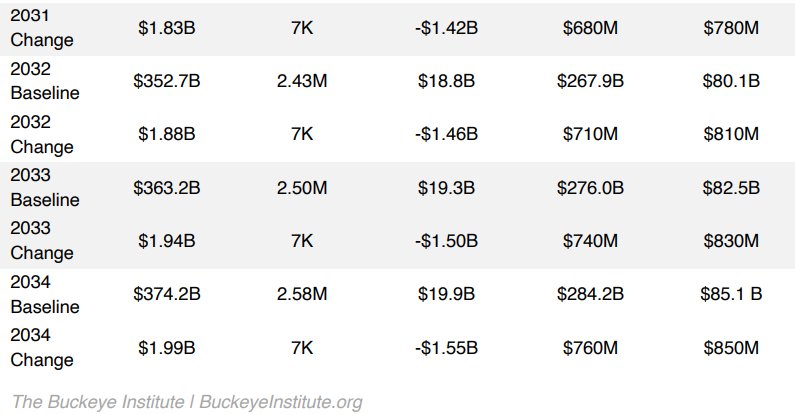

STELA forecasts that once this policy is fully phased in (by 2034), it will generate $1.99 billion in new annual GDP, while spurring $760 million in new consumption and $850 million in new private investment. This economic expansion is driven by the creation of 7,000 new jobs. This dynamic growth provides a substantial feedback effect that offsets the static tax reduction.

Conclusion

Kentucky must continue its pro-growth tax reforms to compete economically with its low-tax neighbors. Historic fiscal health, driven by prudent management and a record-breaking Rainy Day Fund, allows legislative flexibility for responsible reforms and tax refunds. Facing unprecedented workforce mobility, Kentucky cannot afford to maintain a personal income tax that penalizes work and investment. The commonwealth’s move to a flat-tax was a critical first step, and the legislated path to eliminating the personal income tax altogether will be crucial for attracting and retaining the talent and businesses Kentucky needs.

The modeled scenarios confirm that reducing taxes on labor yields more work and more investment, which creates a powerful dynamic feedback effect that generates new state revenue to significantly reduce the net cost of the tax cut. This analysis gives policymakers a better understanding of the tax policy’s full impact and confirms that eliminating Kentucky’s personal income tax remains a fiscally responsible path to sustained economic growth and a more competitive future.

Rea S. Hederman Jr. is executive director of the Economic Research Center and vice president of policy at The Buckeye Institute.

Sai C. Martha is an economic research analyst at The Buckeye Institute.